Motorcycle insurance renewal in Ontario catches most riders off guard, not because the process is complicated, but because it’s easy to treat it like a formality. Your renewal lands in the mail, the number looks familiar, and you sign. The problem is your situation changed between last spring and this one, even if you didn’t notice. A different mileage pattern, a new set of bags, or a move across town can all affect what you’re actually covered for and what you’ll pay.

What changes between year one and year two

Your first renewal is different from every one after it. Year two is when your insurer starts building a real picture of who you are as a rider, and that picture can work for you or against you.

The most important thing that changed: your claims history is now being tracked. Any incident in year one, a tip-over in a parking lot, a minor fender contact, whatever it was, is now part of your record. It follows you when you shop for coverage.

If you progressed from M2 to a full M licence during the year, flag that to your broker. Ontario insurers often rate new riders differently from licensed riders, and that step in your licence carries real financial weight at renewal. Some riders see noticeable rate movement when they hit that milestone. The only way to capture it is to tell your broker it happened.

Modifications are the other common blind spot. You added a windshield in August. New saddlebags in September. Maybe you swapped the exhaust over winter. Every piece of aftermarket equipment that wasn’t declared when you first got coverage is technically uninsured. Not all modifications affect your rate, but they all need to be on record. If you have to make a claim and the adjuster asks what changed on the bike since the policy was written, you want a clean answer.

Did you know?

Harley-Davidson models, particularly touring bikes like the Road Glide and Street Glide, have held their resale value unusually well over the past three years. If you bought your bike in 2023 or 2024, the actual cash value on your policy may be lower than what the bike is actually worth in today’s used market. Worth verifying at renewal.

What to actually look at before you sign

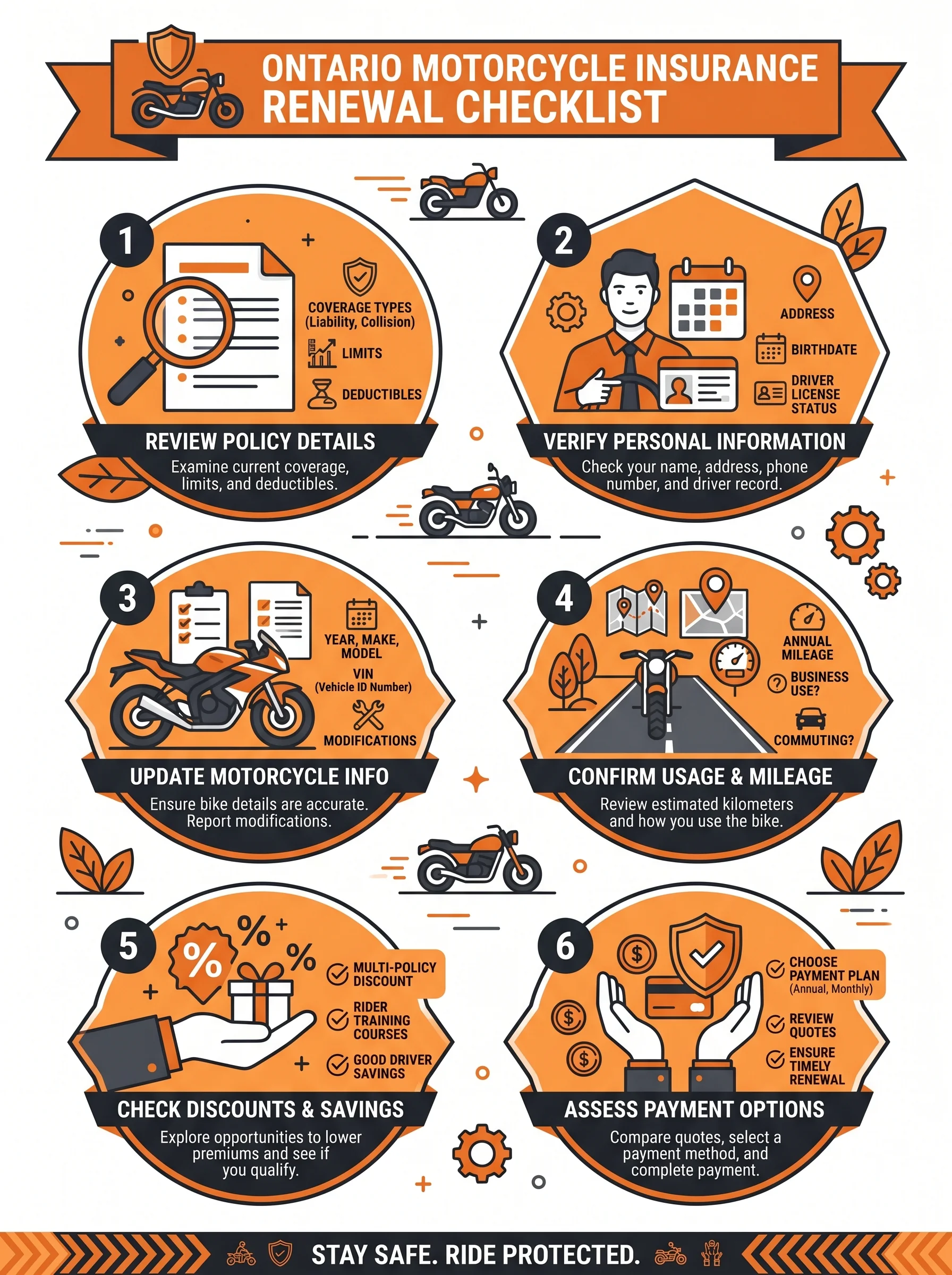

Pull the renewal documents before the due date and look at a few specific things. Most riders skip this step because insurance documents are not enjoyable reading. That is exactly why it’s worth doing.

Replacement cost vs actual cash value

These two coverage types pay out very differently when you file a claim. Replacement cost coverage pays to replace your bike with a comparable one. Actual cash value pays what the insurer thinks the bike was worth at the time of the loss, after depreciation. On a two-year-old Harley that’s appreciated in the used market, those two numbers can be thousands of dollars apart. Know which one you have.

Declared annual mileage

Look at the mileage number on your policy and compare it to what you actually rode last season. Understating mileage to save a few dollars is a bad trade. If you file a claim and the actual odometer reading doesn’t match what you told the insurer, coverage can be affected. If you rode more than declared, update the number. It may not even change your rate much.

Deductible amounts

A higher deductible usually means a lower premium. Whether that trade is smart depends on your financial situation. If a $1,000 deductible would sting but a $500 deductible wouldn’t, that’s worth factoring into your renewal decision. If your financial cushion has changed in the past year, your deductible choice might warrant a second look.

Listed drivers

If your spouse, partner, or adult child rode the bike at any point during the year, they should be listed. Unlisted regular riders are a problem at claim time. This is not a technicality your insurer will overlook.

Endorsements you added

Roadside assistance, gear and accessories coverage, trip interruption. If you added any endorsements in year one, check that they’re still on the renewal. They sometimes fall off between policy versions without anyone catching it. Worth the 30 seconds to confirm.

People often ask: can I change my coverage mid-policy or only at renewal?

You can make changes mid-policy in most cases, but renewal is the cleanest time to do it. Some changes, like adding endorsements or adjusting your declared mileage, can be processed anytime. Others, like switching coverage types, may require a policy rewrite. Call your broker and ask. Riders Plus can walk you through what’s possible.

Questions worth asking your broker at renewal

A renewal call with your broker does not need to be long. But there are a few specific questions worth putting on the table, especially if you’ve had the policy for a year or two.

- Is there anything in my profile from the past year that affects this renewal? A clean riding season can work in your favour. Ask if it did.

- I’ve been a customer for a full year. Is there any adjustment for that, or should I shop around? Loyalty adjustments vary. Some insurers reward it, some don’t. Worth asking directly.

- I made modifications to the bike. Are they on record? List everything: windshield, bags, pipes, foot pegs, whatever changed. Better to declare it now than explain it during a claim.

- What would change if I upgraded to a bigger bike this season? If you’re looking at moving up in the coming months, get a ballpark before you buy. Bigger displacement usually means higher premiums, but the spread varies by model.

- Did I complete a rider training course last year? Some insurers discount for advanced rider training. If you did the course and didn’t mention it, check if it applies to your renewal.

Pro tip

Riders Plus brokers specialize in motorcycle coverage. They’re not going to push you toward a generic auto policy structure. If you have questions that feel too specific or too rider-focused for a general insurance call, that’s exactly what this team handles. Give them a call or get a quote online.

When automatic renewal is the wrong call

Auto-renewing is fine if nothing changed. If anything on this list applies to you, take five minutes and make a call before you sign.

- You moved to a different Ontario city or changed your garage situation. Where you store the bike affects your rate.

- Your bike’s value has gone up significantly. This has been happening with certain Harley models. If you bought used and the market has moved, your actual cash value payout may not reflect what the bike is actually worth.

- You completed an advanced riding course. If you did the Ontario Safety League course or an MSF advanced class and didn’t report it, you may be leaving money on the table.

- Your riding pattern changed. Weekend-only rider to daily commuter is a meaningful change from an insurer’s perspective. So is the reverse.

- You added a rider to the household. If a family member now rides the bike regularly, they need to be on the policy. No exceptions.

Riders Plus Insurance has been working with Ontario motorcycle riders for over 25 years. If your renewal is coming up and you want a second opinion on what you’re looking at, they can walk you through it. No pressure, no hard sell, just a broker who understands how cruiser riders ride.

Questions about your renewal? Get a quote from Riders Plus or call the brokerage directly. They know motorcycle coverage.

Frequently asked questions

Can I add endorsements to my existing policy or do I need to wait for renewal?

Most endorsements can be added mid-policy. Common ones like roadside assistance, gear coverage, and trip interruption can usually be added anytime. Whether a specific endorsement is available mid-term depends on the insurer and the policy type. Your broker can check this quickly.

Does completing a rider training course reduce my premium in Ontario?

Some Ontario insurers offer rate adjustments for advanced rider training. The Ontario Safety League advanced course and certain MSF programs are commonly recognized. Whether your insurer applies a discount and how much it affects your rate varies. Report any courses you completed to your broker and ask directly.

What is the penalty for cancelling a motorcycle policy early?

Early cancellation typically involves a short-rate penalty, meaning you don’t get a prorated refund. The insurer keeps a portion of the remaining premium as a fee. The exact amount varies by insurer and policy. If you’re thinking about cancelling, ask your broker to walk you through what you’d actually get back before you do it.

Does moving to a different Ontario city affect my motorcycle insurance rate?

Yes, location is one of the factors insurers use to rate policies. Some Ontario cities have higher theft rates or accident frequency, which affects premiums. If you moved after your policy was written, report it to your broker at renewal. In some cases it can lower your rate. In others it goes the other way. Either way it needs to be on record.

Trusted by Ontario riders for 25 years. Riders Plus Insurance specializes in motorcycle coverage, not generic auto policy templates. Get a motorcycle insurance quote or call the team directly to talk through your renewal.

Written by

Dave M.

Long-time Harley rider and motorcycle insurance writer with 18 years on the road

Dave M. has been riding Harley-Davidson cruisers since 2006 and writing about motorcycle ownership, insurance, and Ontario road culture for the past decade. Based in Hamilton, he covers the practical side of keeping a bike on the road: what policies actually cover, when to talk to a broker, and how to avoid the mistakes most riders make at renewal time.

join the conversation